Interest rates are fascinating. Understanding how they work is vital whether you’re planning for the future, exploring investment opportunities, or just trying to make your money work harder. Not only are they essential to the financial world, but they also have a big impact on our borrowing and lending decisions and deciding in which bank to keep our deposits and savings.

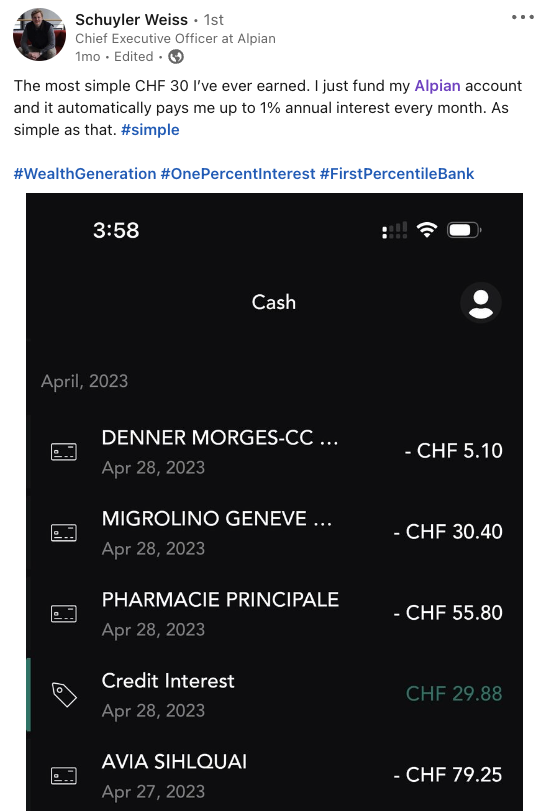

In a recent LinkedIn post, Schuyler Weiss, Alpian’s former CEO, shared a picture of his Alpian account statement, showing that his account had been credited with an interest of CHF 29.88.

He describes this as the “most simple CHF 30 I’ve ever earned. I just fund my Alpian account, and it automatically pays me up an annual interest every month”.

Are interest rates magic? Not really, but their impact on our financial lives is deep-rooted.

What are interest rates?

An interest rate is the cost of borrowing money, or the return earned on lending or saving money.

For example, when you put your money in the bank, it begins to earn interest. This is because banks utilize the funds deposited by individuals like you to constitute reserves, provide loans or make investments.

Essentially, they are paying you for using your money. Similarly, when we borrow money from a bank, we agree to pay back the borrowed amount and an additional amount as interest.

Why are interest rates so important?

As we saw in the example above, each of us can be both a borrower and a lender.

As borrowers, we utilize loans to finance purchases such as homes, cars, education, or everyday expenses through credit cards. Higher interest rates increase the cost of borrowing – we must pay more to access funds.

But as lenders, we can deposit money into banks or invest in financial instruments, earning interest on our capital.

Financial institutions offer interest rates on deposits to attract funds they can lend or invest. Higher interest rates mean we can potentially earn more on our investments and savings.

How are interest rates determined?

Given that interest rates directly impact your life goals (imagine an interest rate so high that you can’t take a loan to pay for your dream home), wouldn’t it be useful to know how these interest rates are set? Here are a few factors that come into play:

1. Borrower’s background

A major concern for lenders can be summed up in one burning question: “Will they return the money?”

The borrower’s creditworthiness, or credit history, plays a crucial role in determining the interest rate. Lenders look at factors like the borrower’s credit history, income stability, and debt-to-income ratio to measure the likelihood of repayment.

Higher-risk borrowers are generally charged higher interest rates to compensate for the increased possibility of defaulting on payments.

2. Loan duration

The period over which the money is lent also affects the interest rate.

Typically, longer-term loans carry higher interest rates than shorter-term loans because longer-term loans expose lenders to potential risks and uncertainties over an extended period, and higher interest rates help minimize these risks.

3. Competitive markets

When there is intense competition among lenders, they may adjust their interest rates to attract borrowers or remain competitive in the market.

If other lenders offer more favourable rates, a lender may need to adjust their rates accordingly to stay competitive.

4. Economic conditions

Factors like inflation, monetary policy, and overall market stability significantly impact interest rates. Central banks, such as the Swiss National Bank, set interest rates at which banks can borrow money, which then serve as reference points for interest rates in the broader economy.

During times of economic growth, interest rates may be higher to manage inflationary pressures. Conversely, central banks may lower interest rates during economic downturns to increase borrowing and economic activity.

The Swiss National Bank raised interest rates. Is this good or bad?

In recent news, you may have come across the Swiss National Bank‘s decision to raise interest rates to combat inflation. If you’re a resident of Switzerland, this move has implications for the interest rates in Switzerland. And for you.

If saving money in Switzerland is a priority, remember that higher interest rates mean higher borrowing costs.

However, they also present an opportunity for more attractive remuneration on your deposits and savings. The exact conditions will vary from one bank to another, depending on the nature of the loan and your circumstances.

Choosing a bank that offers higher interest rates, like Alpian’s high interest rate account, can significantly impact your financial well-being. As interest compounds over time, even small differences in rates can lead to substantial growth over time.

Tapping into the power of interest rates

Knowing how interest rates impact your financial journey can help you make more effective financial decisions as a borrower and a lender.

Choosing the right bank when it comes to keeping your money in savings and borrowing is also crucial. They can empower you to make the most of your financial potential, from your saving goals to maximizing the returns on your investments.

Interest rates are not the only way we can make our money work for us: we can also invest. Interested in investing but a beginner? We invite you to read our Kickstarter Guide with everything you need to get started.