Equity markets —the places where companies like Apple trade their shares— have always captivated investors. They offer daily doses of stories and adrenaline, and the constant excitement leads them to receive the lion’s share of attention from investors.

Although digital assets like cryptocurrencies have become a serious contender for the title of “The most attention-grabbing assets”, equities are still overrepresented across investors’ portfolios.

While several factors explain their popularity —from their sex appeal to ease of access— all the attention might not be entirely justified. Let’s debunk a few myths!

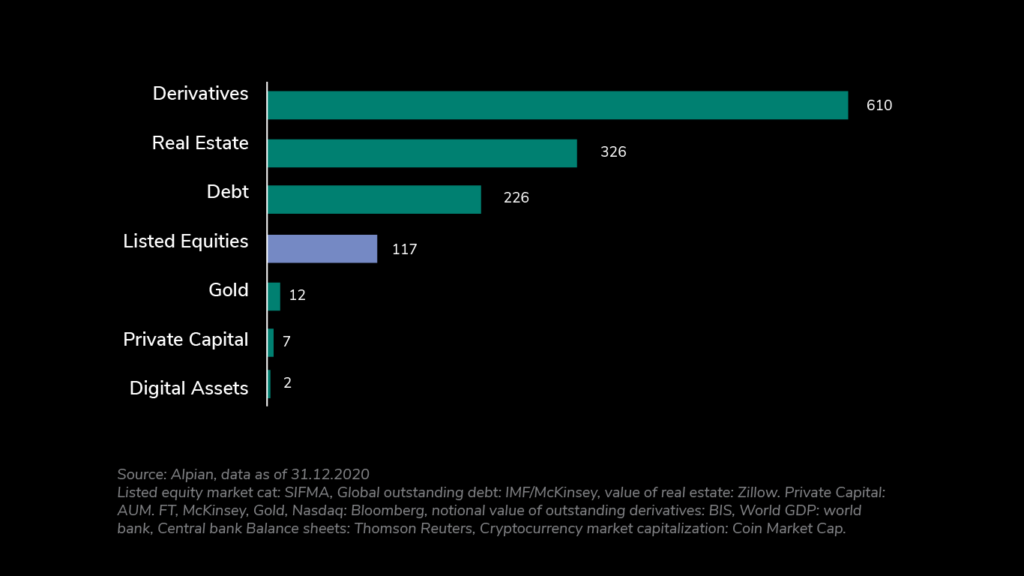

Myth #1: Equity markets are the largest markets

With a market cap of 117 T$ at the end of 2021, the market for listed equities is smaller than bonds, real estate, and debt.

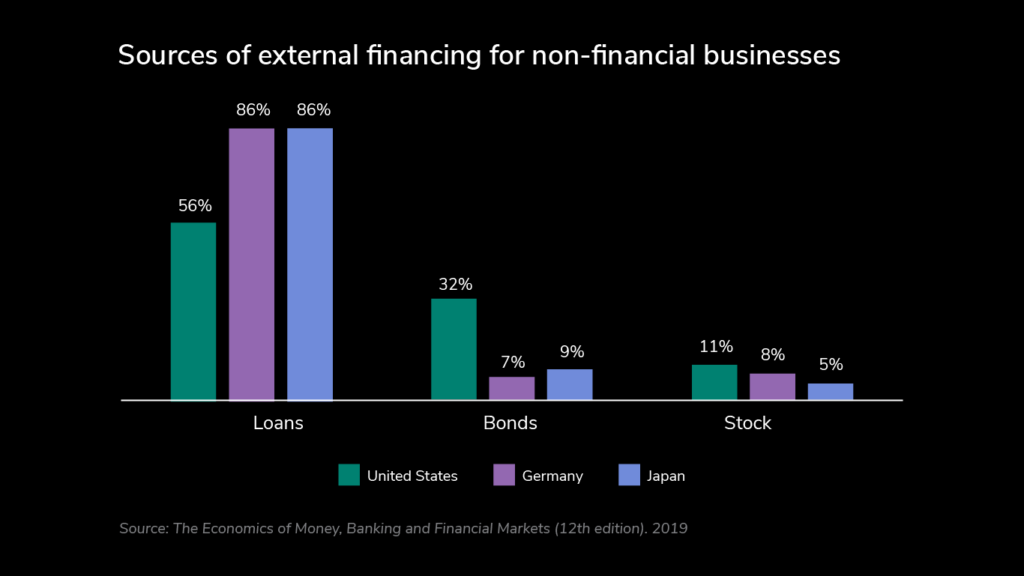

Myth #2: Companies consider the share market the optimal way to raise funds

In fact, most companies choose loans and debt as their primary funding sources.

Of these, debt is the most favored by growing companies. We can see this through the average debt-to-equity ratio (which measures the relative importance of debt and equity that a company uses to finance their operations and assets): it’s around 1.5 for companies in the S&P 500.

Myth #3: Most companies perform well

Listing on the share market is not a guarantee of future performance. While a handful of major success stories —like the FANG companies— captivate investors, these do not represent the market as a whole. Let’s take the Nasdaq composite as an example:

Not all of the 4600 companies have the same weight within the index. Microsoft and Apple represent more than 20% of its size, and it’s often these large companies that drive the performance of the index as a whole (in fact the top 100 companies account for over 90% of the movement of the index).

If we take a year like 2021, the Nasdaq composite recorded a positive performance of 22%. But if you scratch the surface, more than half of the companies in the index recorded a negative performance.

Nearly all stock exchanges contain highly leveraged and unprofitable companies (we call them “zombies”), and in 2019 this was determined to be around 10% of the total market in the U.S.

Myth #4: The biggest companies in the world are all publicly traded

The first thing to note is that listed companies are the tip of the iceberg.

While the number of listed companies is around 43,000 as at the end of 2020 (Listed domestic companies, total | Data (worldbank.org)), the number of unlisted companies is measured in tens of millions.

There are more than 300 million businesses worldwide (Dun & Bradstreet in 2021), and some of the largest and most lucrative are privately held.

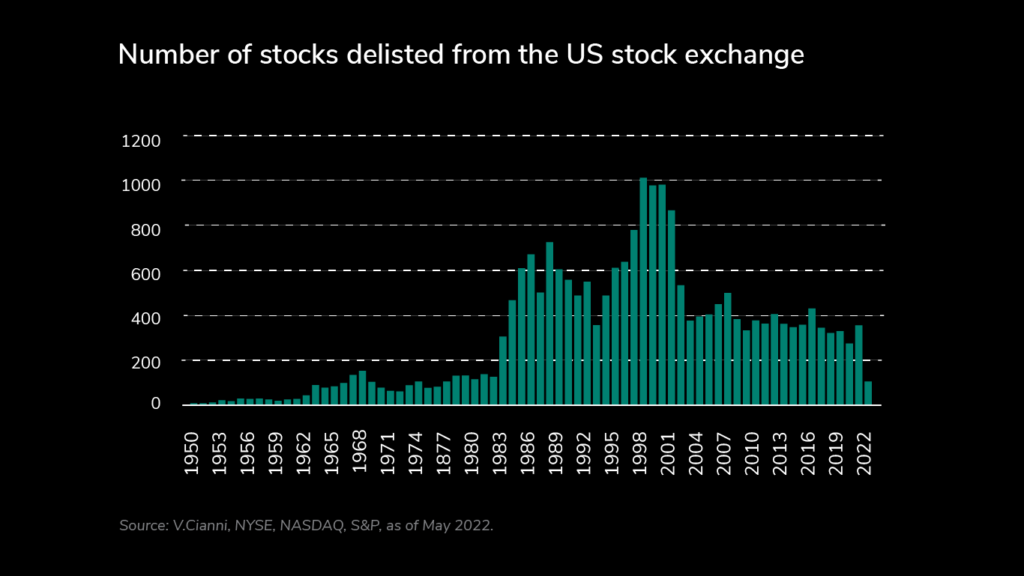

Myth #5: Once listed, always listed

Delisting —the act of removing stock from the stock exchange— occurs for several reasons: insufficient market cap, bankruptcy, failure to comply with regulatory requirements, and acquisition (e.g. Elon Musk considering taking Twitter private), to name a few.

This happens more often than we think: Between 2019 and 2020, 179 companies were delisted from US stock exchanges. And since 1950, more than 22,000 companies have been delisted.

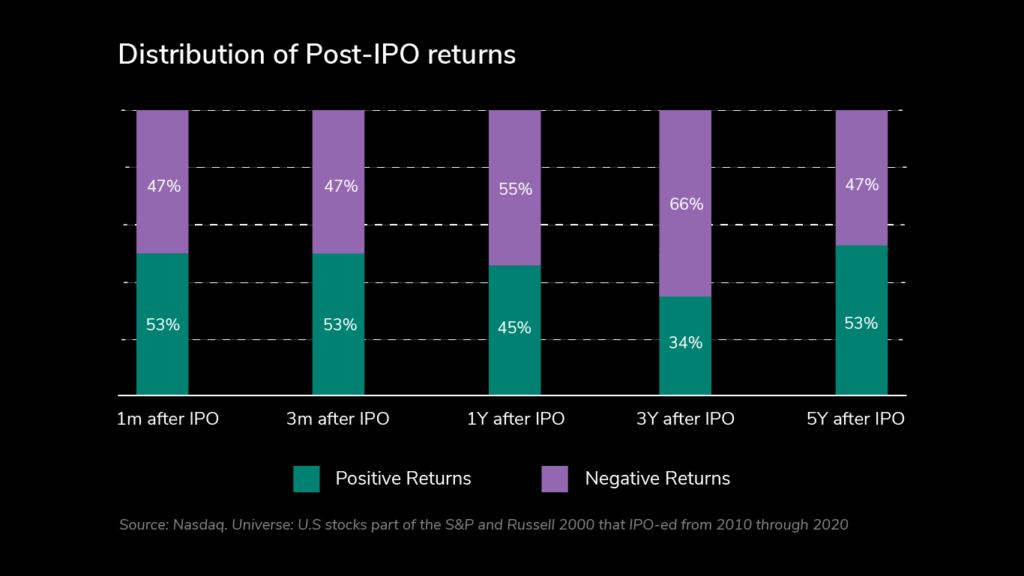

Myth #6: IPOs are profitable

Many investors pay more attention to IPOs (Initial Public Offerings) than any other event. While their excitement pushes prices high at the time of the stocks being introduced to the market, this is typically followed by decreased interest over time.

Myth #7: Some companies are too big to fail

Investors have an inherent bias towards size, this culminates in the idea that big and successful companies cannot fail.

While successful companies tend to stay in the spotlight for a long time, they often disappear once things turn south. Think about it – we have all forgotten a company like Blockbuster that quietly liquidated.

List of corporate collapses and scandals – Wikipedia

Enron and the 24 Other Most Epic Corporate Downfalls of All Time | GOBankingRates

Putting aside collapses and scandals, no companies are genuinely “immortal”. While there are a few supercentenarian companies (The Japanese construction company has been operating for over 1,400 years), most have a lifecycle. They are born, grow, mature, and decline.

An interesting report from McKinsey, recently suggested that the average lifetime of companies is decreasing: In 1958, the average lifespan of companies listed in Standard & Poor’s 500 was 61 years. Today, it is less than 18. McKinsey believes that in 2027, 75% of the companies currently quoted on the S&P 500 will have disappeared.

What do we make of all this?

As always in finance, understanding the markets you trade in is important.

Headlines do not shed enough light to be valuable, and financial news and data sources are naturally biased toward the largest and most attention-grabbing companies. Not only does this landscape favor equity markets over other asset classes, but the lean toward excitement can also easily impair an investor’s judgment.

Considering the bigger picture of investment opportunities could help you to build more objective investment analyses and access a wider range of options.

Disclaimer:

The content of any publication on this website is for informational purposes only.