Transactions are a fundamental part of economic activity. With millions of international transactions taking place daily, SWIFT codes provide a standardized way to identify banks and ensure that money transfers are always made to the right account. But what does SWIFT actually stand for and what do “normal/non-banking experts” need to know?

Nowadays, almost every organization relies on the efficient working of the SWIFT network for its day-to-day operative functions. Businesses use SWIFT to send money to other countries, banks send and receive money from clients through SWIFT, and financial institutions based in one country have clients from different parts of the world who send money to them through SWIFT.

The SWIFT Story

SWIFT stands for Society for Worldwide Interbank Financial Telecommunications. In other words, SWIFT is a secured telecommunication network by which a financial institution in one country can communicate with its branches or correspondent institutions virtually anywhere in the world, except of course banned or sanctioned countries.

Since its founding in 1973, it has had its headquarters in Belgium. It is members owned, among which are many European and American banks. The company is overseen by the National Bank of Belgium, in partnership with major central banks around the world – including the US Federal Reserve and the Bank of England. It has now over 11000 members and its presence in over 200 countries daily.

But how does SWIFT actually work?

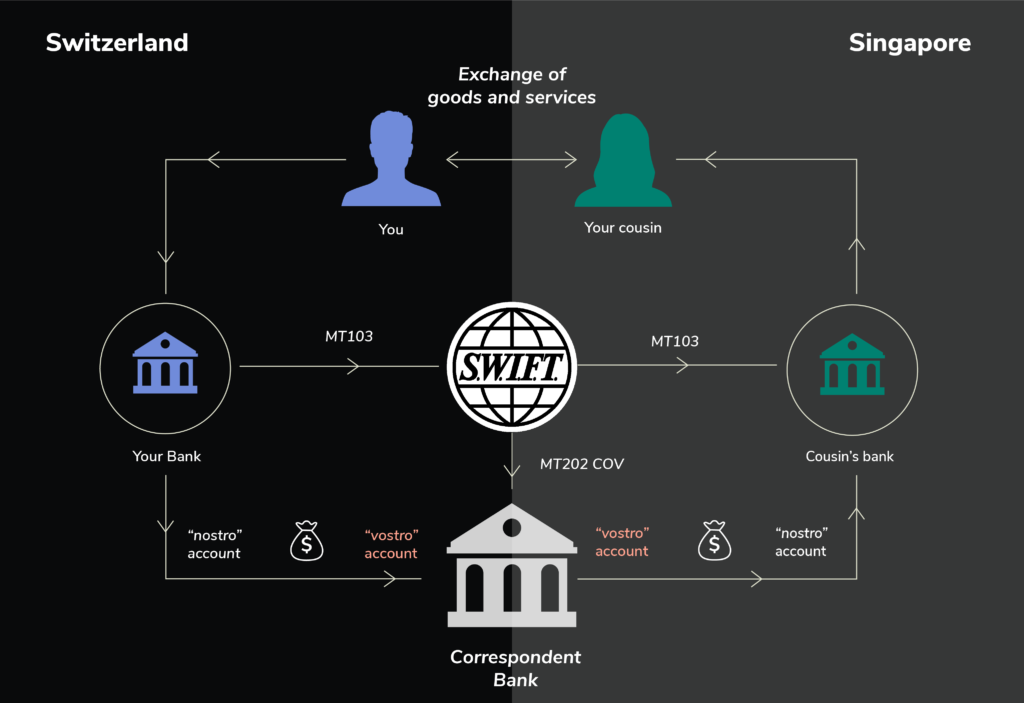

To make it simple, let’s take the following payment example:

You reside in Switzerland and want to transfer some money to your cousin in Singapore. You provide your bank with your cousin’s IBAN or account number, BIC and the amount to be paid.

Let’s assume that your bank in Switzerland has a bilateral agreement with another bank in Singapore acting as a correspondent bank. Here’s what happens next:

- Your Swiss bank debits your account and sends a SWIFT message MT103 to your cousin’s bank with all the necessary payment details.

- Your Swiss bank sends an MT202cov message to its correspondent bank (called also intermediary bank) in Singapore to perform the transfer of the fund.

- The correspondent bank debits the account held by your Swiss bank (Nostro) and credits the account held by your cousin’s bank in Singapore.

- Your cousin’s bank receives the money and credits the amount to your cousin’s account.

If the banks don’t have an established relationship, they won’t have a Nostro/Vostro account with each other. In this case, SWIFT will send the message through one or more intermediary banks that do have shared Nostro/Vostro accounts until the final beneficiary’s bank can be reached.

As you can probably tell by now SWIFT is used worldwide and daily by financial institutions and people like you and me.

In short, financial institutions from banned countries cannot use the SWIFT network, and therefore cannot do business as easily as a non-banned financial institution.

So, what happens when there is a ban on a country?

In short, financial institutions from banned countries cannot use the SWIFT network, and therefore cannot do business as easily as a non-banned financial institution.

This includes the settlement of large transactions on commodities, such as oil, and gas, but also basic commodities like cereal or toys. So, if no settlement can occur, no delivery of goods can happen either.

Is there an alternative to SWIFT?

Yes, but not quite. China and Russia introduced their own alternative to SWIFT in 2015 and 2018 respectively. China’s Cross-Border Interbank Payment System (CIPS) settles cross-border RMB transactions while Russia’s System Transfer of Financial Messages (SPFS) settles cross-border RUB transactions. Both systems are limited in terms of services and currency and can’t replace SWIFT, which accounts for more than 80% of international transactions.

SWIFT and the future

Today, the SWIFT system is used worldwide, carries information vital to international transactions between banks, and is now critical for the global economy. Even with the presence of cryptocurrencies and blockchain ledger systems, there are indications that SWIFT is not working against them, but rather working towards solutions that make international payments smoother for digital currencies.

***

Disclaimer:

The content of any publication on this website is for informational purposes only.